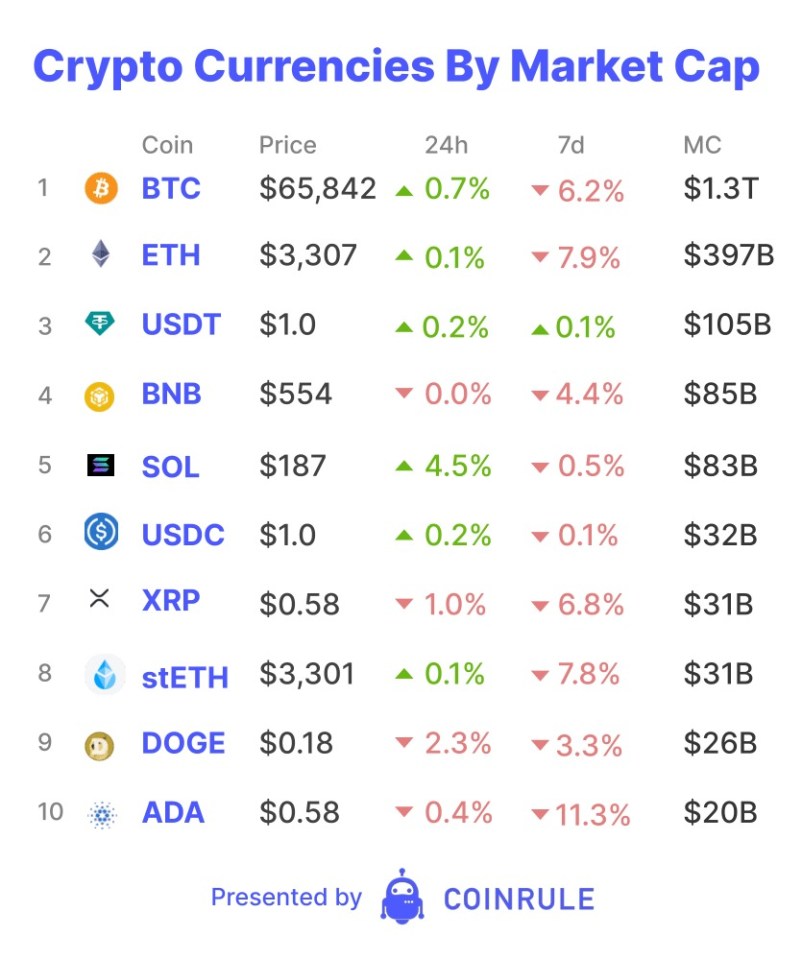

On Tuesday, the market experienced a sharp decline due to some of the $2 billion of Bitcoin within the United States Department of Justice’s wallet being moved. The wallet’s contents came from seizing 50,000 Bitcoin stolen from the dark web site, Silk Road. The market noticed an initial test transaction of 0.001 ($69) Bitcoin to Coinbase Prime, suggesting an impending sell-off. Thankfully, the US appears to be dollar-cost-averaging out, with them sending only $130 million to Coinbase. The decline caught traders off guard, with over $500 million being liquidated across Tuesday, according to CoinGlass. The move reset funding rates back to more neutral levels on most assets.

However, lower funding rates do not suit the market’s latest token – Ethena. In a previous article we discussed the launch of Ethena’s DeFi protocol that features their stablecoin, USDe. The staked version, sUSDe, currently provides yields of over 35% APY. The protocol generates yield by holding staked Ethereum. It earns additional yield by capturing positive funding rates via shorting an equivalent amount of Ethereum on futures markets. It uses these positions as collateral to back USDe and maintain its peg to $1.

Since Ethena’s creation, there has been significant discussion around its success and viability. Ethena has attracted nearly $2 billion to its stablecoin – becoming one of the highest revenue generating protocols, not including major layer 1s.. It has also caused a credit rating war within DeFi. MakerDAO, a stablecoin issuer, approved a proposal last Friday to accept $100 million of USDe as collateral to borrow DAI, its stablecoin. MakerDAO has also now suggested they will increase this ceiling to $600 million, with $1 billion also a future possibility. According to Bankless, currently only 2% of DAI’s supply is collateralised by USDe lending. Yet, these loans are producing 36% of annual yield and represent 10% of Maker’s potential 2024 revenues.

However, some protocols view Ethena as a potential risk to DeFi stability. Contributors to Aave, a lending protocol, have created proposals to remove DAI’s collateral status from the protocol. Aave’s founder stated Aave no longer aligns with Maker due to its increasing appetite for risk. However, there are speculations the move is more strategic, with Aave potentially trying to hinder a competitor to their own stablecoin, GHO.

As with any investment, the greater the returns, the higher the risk. However, the fact Ethena’s stablecoin yields are among the highest, does it mean the risks are unmanageable? As with all crypto protocols, any real test may only come during a bear market.